Basel standards and developing countries: A difficult relationship

In today’s world of globalised finance, regulators in developing countries have to weigh up the international ramifications of their decisions. This column presents the results of a research project which combines cross-country panel analysis and in-depth case studies of the political economy of the adoption of Basel II/III in the developing world. It finds that regulators in developing countries do not merely adopt Basel II/III because these standards provide the optimal technical solution to financial stability risks in their jurisdictions; concerns about reputation and competition are also important.

In the wake of the Global Crisis, significant regulatory reforms have been undertaken, most prominently, the Basel III reforms, which tighten capital requirements and introduce liquidity requirements and macroprudential tools. These reforms were agreed upon by the 28 members of the Basel Committee on Banking Supervision (hereafter ‘Basel Committee’), representing major advanced and emerging economies. While in principle only member countries are obliged to adopt and implement these standards, they are widely seen as ‘best-practice’ regulatory standards.

Many non-members of the Basel Committee thus adopt Basel banking standards even though they have no seat at the standard-setting table. Implementation of the first Basel standard is almost ubiquitous, and the newer two standards – Basel II and III – have found widespread acceptance beyond the perimeter of the Basel Committee. Data from the Financial Stability Institute (2015) at the Bank of International Settlements show that 90 out of 100 surveyed non-member jurisdictions have implemented Basel II at least partially or are in the process of doing so. Moreover, 81 jurisdictions reported that they had taken steps towards the implementation of at least one component of Basel III.

A recent research project titled "Developing countries navigating global banking standards" combines cross-country panel analysis and in-depth case studies of the political economy of the adoption of Basel II/III. It provides important insights into the factors that explain why or why not regulators in developing countries adopt and implement international regulatory standards.

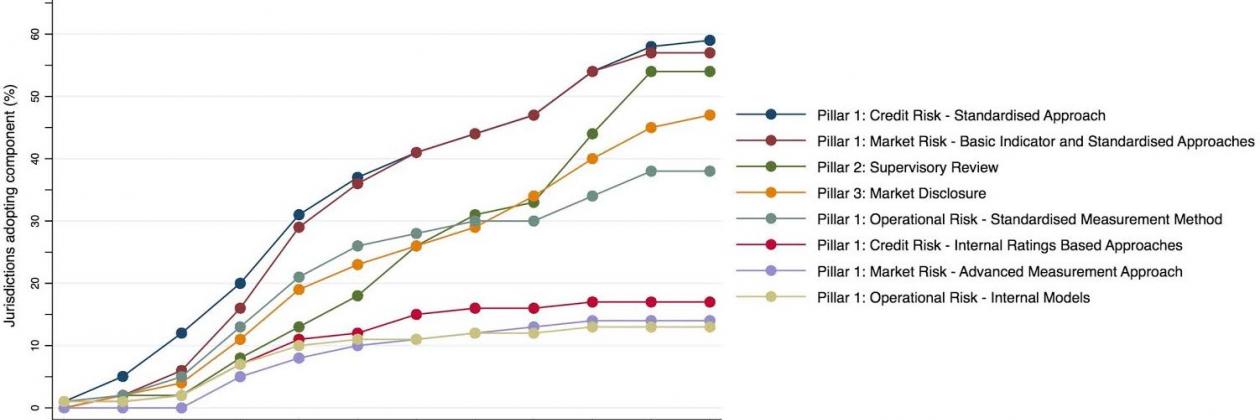

Figure 1 Basel II adoption by non-members

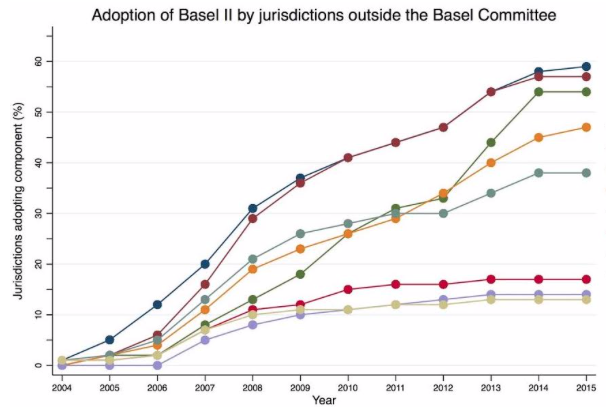

Regulators in developing countries are typically selective adopters, choosing some components of Basel standards while eschewing others (Jones and Zeitz 2017). In particular, regulators are more likely to adopt the simpler Basel II standard approaches to credit, market and operational risk instead of much-disputed advanced approaches that rely on internal risk models by banks (Figure 1). Similarly, Figure 2 indicates that simple components of Basel III such as the new definition of capital and the leverage ratio are more popular than complex requirements such as the liquidity ratios or the countercyclical buffer.

Figure 2 Basel III adoption by non-members

Reputation and competition concerns drive Basel implementation

Regulators in developing countries do not merely adopt Basel II/III because these standards provide the optimal technical solution to financial stability risks in their jurisdictions. Instead, regulatory decisions are also driven by concerns about reputation and competition (Jones and Zeitz 2018). We find that the following factors drive the adoption of Basel II/III:

- Signalling to international investors. Incumbent politicians may adopt Basel standards in order to signal sophistication to foreign investors. For example, in Ghana, Rwanda, and Kenya, politicians have advocated the implementation of Basel II and III, and other international financial standards, as part of a drive to establish financial hubs in their countries. However, adoption can be selective, as seen in the case of Kenya. While the Central Bank of Kenya has sought to improve the regulatory and supervisory framework and has looked to international standards as the basis for these reforms, it has implemented the standard approach of Basel II while eschewing the advanced components based on internal ratings. Similarly, liquidity requirements in Kenya are simpler than those of Basel III but arguably better tailored to the characteristics of the domestic banking system.

- Reassuring host regulators. Banks headquartered in developing countries may endorse Basel II or III as part of an international expansion strategy, as they seek to reassure potential host regulators that they are well-regulated at home. We see this at work in Nigeria, where large domestic banks have championed Basel II/III adoption at home as they seek to expand abroad. Their regulatory fervour has been met with reluctance among politicians who fear that a rapid regulatory upgrade may put weaker local banks in jeopardy.

- Facilitating home-host supervision. Adopting international standards can facilitate cross-border coordination between supervisors.1 In Vietnam, for example, regulators were keen to adopt Basel standards as their country opened up to foreign banks, to ensure they had a ‘common language’ to facilitate the supervision of the foreign banks operating in their jurisdiction.

- Peer learning and peer pressure. Even while acknowledging the shortcomings of Basel II and III, developing countries regulators often describe them as international ‘best practices’ or ‘the gold standard’ and there is strong peer pressure in international policy circles to adopt them. In the West African Economic and Monetary Union, for example, regulators at the supranational Banking Commission are planning an ambitious adoption of Basel II and III with the support and encouragement of technocratic peer networks and the IMF. Domestic banks, however, have limited cross-border exposure and show little enthusiasm for the regulator-driven embrace of Basel standards.

- Technical advice from the IMF and the World Bank plays an important role in shaping the incentives for politicians and regulators in developing countries. While the Financial Stability Assessment Programs are designed to merely evaluate the regulatory environment of client countries against a much more basic set of so-called Basel Core Principles, we find evidence that the Fund and the Bank motivate regulators in developing countries to engage in Basel II and III adoption, in some cases with explicit recommendations.

Explaining cross-country variation

As developing countries differ greatly in the nature of their financial sectors, their political economy dynamics, and level of integration into global finance, we find that regulators are taking very different approaches to Basel II/III adoption (Figure 3).

Figure 3 Basel II/III adoption in 11 low- and lower-middle-income (LMIC) case countries

Among our eleven case study countries, Ethiopia lies at one extreme, as it has chosen to not adopt Basel II or III. The relative isolation of Ethiopia’s banking sector and lack of multinational banks gives domestic banks few competitive incentives to adopt the Basel framework. Meanwhile, Ethiopia’s government has a strong preference for political control over the financial industry as it seeks to emulate the example of East Asian ‘tiger’ economies, for whom policy-directed finance represented a key tool in the pursuit of rapid industrialisation. Thus, in the absence of strong technical, competitive, or reputational incentives, Ethiopia currently has no domestic champions for Basel II/III adoption (Weis 2017).

On the other extreme, Pakistan has a very high level of adoption of Basel II and III. In the 1990s and early 2000s, the adoption of Basel II was driven first by a policy of promoting financial services, and then by banking sector regulators who sought to implement best practices. As banks have internationalised over the past decade, they have championed the implementation of Basel III. Pakistan is one of the few cases where all three major actors in the decision process related to the adoption of international standards – politicians, regulators, and banks – have become internationally oriented, leading to substantive compliance with international banking standards (Naqvi 2017).

Bolivia, on the other hand, has experienced competing influences. Bolivianregulators are deeply engaged in international policy discussions and regard Basel III as the gold standard for banking regulation, while the Ministry of the Economy and Public Finances is more concerned with financial inclusion and domestic development than with attracting foreign capital, thus grafting onto the draft legislation significant interventionist policies such as interest rate caps and credit targets to certain economic sectors (Knaack 2017).

In summary, the different case studies show the importance of the interests of different stakeholders in the financial system, most prominently bankers, regulators and politicians.

Choosing the optimal approach – options for regulators in developing countries

What steps can financial regulators in LMICs take to harness the prudential, reputational and competitive benefits of global banking standards, while avoiding the implementation risks and challenges associated with wholesale adoption? Our research highlights several options for regulatory agencies in LMICs. Here we focus on two that relate directly to the findings discussed above.

- Identify incentives and distinguish between prudential, reputational, and competitive motives. In deciding whether, to what extent, and how to implement Basel II and III, regulators need to establish not only what is optimal from a technical perspective, but also how important reputational and competitive concerns are for their jurisdiction. Our research showsthat three groups of domestic stakeholders shape the degree of Basel standards adoption in developing countries – incumbent politicians, regulators, and the banking sector. The incentives of each group of stakeholders may or may not align. Incumbent politicians keen on the promotion of the country as a financial services hub, for example, may discount the costs that an off-the-shelf Basel adoption entails both for the regulatory authority and the banking sector. On the other side, internationally oriented domestic banks may push the government to embrace Basel II/III not out of prudential concerns but because they expect to reap reputational and competitive benefits, including vis-à-vis smaller domestic rivals.

- Tailor Basel standards to national circumstances. Regulatory agencies outside the Basel Committee on Banking Supervision are not bound by its rules and not subject to peer review procedures. Regulators in the financial periphery can use this freedom to adapt global standards to meet domestic regulatory needs, as some but not all are already doing.

References

Beck, T, C Silva Buston and W Wagner (2017), "The economics of cross-border supervisory cooperation", CEPR discussion paper 12764.

Financial Stability Institute (2015), FSI survey - Basel II, 2.5 and III implementation, Basel: Bank for International Settlements.

Jones, E and A O Zeitz (2018), "Regulatory convergence in the financial periphery: How interdependence shapes regulators’ decisions", Global economic governance programme working paper, Blavatnik School of Government, University of Oxford.

Jones, E and A O Zeitz (2017), "The limits of globalizing Basel banking standards", Journal of Financial Regulation 3(1): 89-124.

Knaack, P (2017), "The political economy of Basel implementation in Bolivia", Global economic governance programme working paper, Blavatnik School of Government, University of Oxford.

Naqvi, N (2017), "The political economy of Basel implementation in Pakistan", Global economic governance programme working paper, Blavatnik School of Government, University of Oxford.

Weis, T (2017), "The political economy of Basel implementation in Ethiopia", Global economic governance programme working paper, Blavatnik School of Government, University of Oxford.

Endnotes

[1] Beck et al. (2017) have shown a significant increase in cross-border supervisory cooperation over the past decade.