Author: Radha Upadhyaya

Summary

Kenya is a high adopter of Basel standards relative to other countries in our case study sample. Kenya’s adoption of Basel standards is due to the alignment of politicians, regulators and banks, in addition to donor interests. The impetus for Basel implementation has come from the Central Bank of Kenya (CBK), which is highly independent, internationally oriented and very receptive to international policy ideas. Since 2003, the incumbent politicians have also been internationally oriented and keen to adopt the latest international standards. Meanwhile, as the banking sector is relatively well capitalised, there has been little opposition from banks, with some international and large local banks being mildly in favour of Basel II and III adoption.

Kenya thus exemplifies an international consensus among actors in favour of Basel adoption (Type 5). In the Kenyan case, the regulator is the driving force, and it receives support from internationally oriented politicians and banks. Although they were early movers, Kenyan regulators have also taken a selective approach to implementation. However, interviewees suggest that this was the result of a lack of resources rather than lack of intent and therefore not a form of mock compliance.

Political economy background

The Kenyan economy is largely dependent on agriculture, which contributed to 30% of GDP in 2015, and while manufacturing growth is sluggish, the services sector has been performing well. Kenya has a long history of a diversified banking sector with both foreign and local banks and an established stock market with international and local private banks continuing to operate since independence. This combined with innovation in the banking sector (mobile banking) has contributed to major gains in financial inclusion.

| GDP per capita (current USD) | 1,508 |

|---|---|

| Bank assets (current USD) | 31bn |

| Bank assets (% of GDP) | 43.8 |

| Stock market capitalisation (% of GDP) | 50 |

| Credit allocation to private sector (% of GDP) | 32.7 |

| Credit allocation to government (% of GDP) | 13.7 |

| Polity IV score (2017) | 9 |

Note: All data is from 2016 unless otherwise stated

Source: FSI Database, IMF (2018); GDI Database, World Bank (2017); Central Bank of Kenya (2015); Handjiski et al (2016); Polity IV (2014)

Basel implementation to date

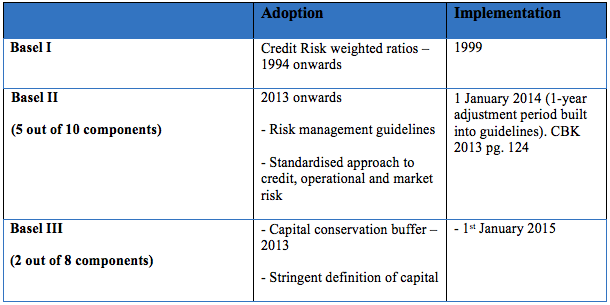

While Kenya was a relatively late adopter of Basel I, it has made significant efforts to adopt and implement Basel II and Basel III from 2006 onwards. By 2007–2008, the CBK was developing a framework and preparing the prerequisite supervisory infrastructure to implement Basel II and new prudential guidelines were issued in 2013, including many elements of Basel II and some of Basel III. During the same period, Kenya’s compliance with the Basel Core Principles increased significantly. This said, there is evidence that despite good adoption of the regulations, enforcement did not happen in full, particularly before 2015.

Political economy of Basel implementation

Kenya is a relatively high adopter of Basel standards due to the alignment of government (politicians and regulators), banking sector and donor interests. These groups share the view that Basel standards implementation is essential to the achievement of the country’s Vision 2030.

With the election of President Mwai Kibaki in 2003, the government embarked on an extensive reform agenda which included financial reforms. While the early impetus for Basel adoption came from the perceived need to clean up a banking sector that was fraught with nonperforming loans, more recent moves have been motivated by the desire to create an internationally recognised financial hub. With the help of international consulting firms, the government prepared a plan to turn Nairobi into a regional finance hub by establishing the Nairobi International Financial Centre (NIFC). Basel II and III implementation is regarded by the government as a key ingredient to endow Kenya with regulatory status and competitive advantage in the eyes of international investors. Furthermore, Treasury and Central Bank officials had internalised some of the messages coming from the IMF and the World Bank in support of Basel II and III implementation. From 2003 onwards, the two institutions developed the Financial and Legal Sector Technical Assistance Programme (FLSTAP), a broad-based lending programme to assist the Kenyan government in identifying weaknesses in the financial sector. Although there was disagreement between the government and World Bank on the privatisation of government-owned banks, there was genuine enthusiasm among government officials for the regulatory agenda of the FLSTAP, which included the adoption of international financial standards.

The driving force behind the implementation of Basel and other international banking standards has been the Central Bank of Kenya, which has enjoyed a high level of autonomy, giving it the leeway needed to adopt and implement Basel standards. The CBK’s determination to implement Basel standards is the result of three factors: 1) the extreme fragility of the banking sector in the early 2000s; 2) the view that improved regulation is essential to fostering growth within the financial sector; and (3) the international orientation of CBK Governors, who have been influenced both by the IMF and World Bank, and their peers. The CBK officials are also involved in several international networks and have been exposed to high levels of international training on regulatory issues.

Neither international nor private banks lobbied directly for Basel standards but they were not opposed to them. International banks were already at different stages of adopting Basel II and III due to their head office reporting requirements. Large local banks that are expanding across the region regard Basel standards as a ‘defence mechanism’ that allows them to set up business in other jurisdictions without suspicion. Interviews showed that smaller local banks were generally well capitalised, but struggled with adopting the risk-based guidelines, mainly because of human resource constraints.

Kenya has not adopted the standards fully but selected those parts of Basel II and Basel III that are relevant to its circumstances. In terms of our analytical framework, the dynamics in Kenya illustrate how regulator-driven convergence can lead to implementation when supported by politicians and banks. Perhaps because the regulator has greater institutional capacity than in countries like those in the West African Economic and Monetary Union (WAEMU) and Rwanda, and so understands the challenges posed by Basel standards, it has taken a more selective approach to implementation.